- Entrepreneurial Wisdom

10 Essential Tasks to Complete Before Starting Your Business

Starting a business is both exhilarating and daunting. As a new entrepreneur, you’ll likely feel the pressure of juggling multiple responsibilities, all while navigating unfamiliar territory.

While there’s no shortcut to success, careful planning and focusing on the right tasks early on can significantly increase your chances of building a thriving business.

This article outlines 10 essential tasks you must complete before launching your venture.

By tackling these tasks, you’ll lay a strong foundation for your business and set yourself up for long-term success.

1. Find your Idea and Understand the Market

Get Your Business Idea

If you already have your idea, skip this. If not, you can look at our article on 4 Ways To Find Your Business Ideas.

Understanding the Industry

- Define Your Niche: Focus on industries or types of sales (B2B, B2C, SaaS, etc.) where you have the most experience.

- Build a Portfolio: Showcase your success stories with tangible results.

- Network Aggressively: Attend industry events, leverage LinkedIn, and connect with potential clients.

- Set Your Rates: Pricing should reflect your expertise and your value to clients.

Analyzing Competitors

No matter how unique your business idea is, there’s a high chance others have already explored similar concepts.

Conduct a comprehensive SWOT competitor analysis (use the framework below) to identify your competitors, what they offer, and how they operate. Examine their strengths and weaknesses, pricing strategies, marketing efforts, and customer reviews.

This analysis will help you identify gaps in the market that your business can fill.

Oscar Hackett

2 x Founder, SaaS Sales Leader and Investor. Love all things tech and helping people grow their own companies.

Get 500+ Hours of Research and business ideas into your inbox every week.

2. Identify and Understand Your Target Audience

Knowing your target audience is key to developing effective marketing and sales strategies. Start by creating detailed buyer personas that outline the characteristics of your ideal customers.

Consider factors such as age, gender, income level, education, and geographic location. Additionally, consider psychographic factors like lifestyle, interests, and values.

B2C vs. B2B Considerations

Determine whether your business is business-to-consumer (B2C) or business-to-business (B2B). Each model has its nuances, affecting everything from marketing approaches to sales cycles. For B2C businesses, focus on emotional appeal and convenience. For B2B businesses, prioritize building relationships and demonstrating ROI.

Tailoring Your Offerings

You can clearly understand your audience and tailor your products or services to meet their specific needs. Ensure that your offerings provide tangible benefits and solve real problems for your customers.

This customer-centric approach will attract new clients and foster loyalty among existing ones.

Get 500+ Hours of Research and business ideas into your inbox every week.

3. Develop a Strong Mission Statement

A strong mission statement is the cornerstone of your business. It defines your purpose, values, and long-term goals, serving as a guiding light for decision-making. Reflect on why your business exists and what impact you want to make in the world. Your mission statement should be concise, inspirational, and resonate with both your team and customers.

Differentiating Your Business

In a crowded marketplace, differentiation is crucial. Your mission statement should highlight what sets your business apart from competitors. Whether it’s superior quality, innovative solutions, or exceptional customer service, make it clear how your business stands out.

Aligning with Long-Term Goals

Your mission statement should align with your long-term vision for the business. Consider how your goals may evolve over time and ensure your mission statement remains relevant. As your business grows, revisit and refine your mission to reflect any changes in direction.

4. Choose the Right Legal Structure

Types of Business Structures

Selecting the appropriate legal structure is a critical step that affects your taxes, liability, and ability to raise capital. Common business structures include sole proprietorships, partnerships, limited liability companies (LLCs), and corporations.

Each structure has pros and cons, so choosing one that aligns with your business goals and risk tolerance is important.

Tax Implications

Different business structures come with varying tax obligations. For example, sole proprietorships and partnerships offer pass-through taxation, where profits are taxed individually.

On the other hand, corporations face double taxation but offer more protection against personal liability. Consult with a tax advisor to understand the tax implications of each structure.

Legal Requirements and Registration

Once you’ve chosen a structure, you’ll need to register your business with the appropriate state and local authorities.

This process typically involves filing articles of incorporation (for corporations), obtaining an employer identification number (EIN), and applying for necessary licenses and permits. Compliance with legal requirements is essential to avoid fines and penalties.

Get 500+ Hours of Research and business ideas into your inbox every week.

5. Map Out Your Finances

Starting a business requires a significant financial investment. Begin by estimating your startup costs, which may include expenses such as equipment, inventory, marketing, and office space. Having a clear understanding of your financial needs will help you create a realistic budget.

Exploring Funding Options

If you don’t have enough personal savings to cover startup costs, explore various funding options. Common sources of capital include personal savings, loans from friends and family, angel investors, venture capitalists, and small business loans. Each option has its advantages and disadvantages, so weigh them carefully before making a decision.

Creating a Financial Plan

A financial plan is a roadmap that outlines how you will manage your business’s finances. It should include projected income and expenses, cash flow statements, and break-even analysis. Regularly review and update your financial plan to ensure your business remains financially healthy.

6. Create a Comprehensive Business Plan

A business plan is a detailed document that outlines your business’s goals, strategies, and financial projections. It serves as a blueprint for your business and is essential for securing funding and attracting investors. Key components of a business plan include:

- Executive Summary: A brief overview of your business and its objectives.

- Company Description: Information about your business, including its mission, vision, and values.

- Market Analysis: An in-depth analysis of the market, including industry trends, target audience, and competitor analysis.

- Organization and Management: Details about your business’s organizational structure, including key team members and their roles.

- Products and Services: A description of the products or services you offer, including pricing and competitive advantages.

- Marketing and Sales Strategy: A plan for attracting and retaining customers.

- Financial Projections: Detailed financial forecasts, including projected income, expenses, and cash flow.

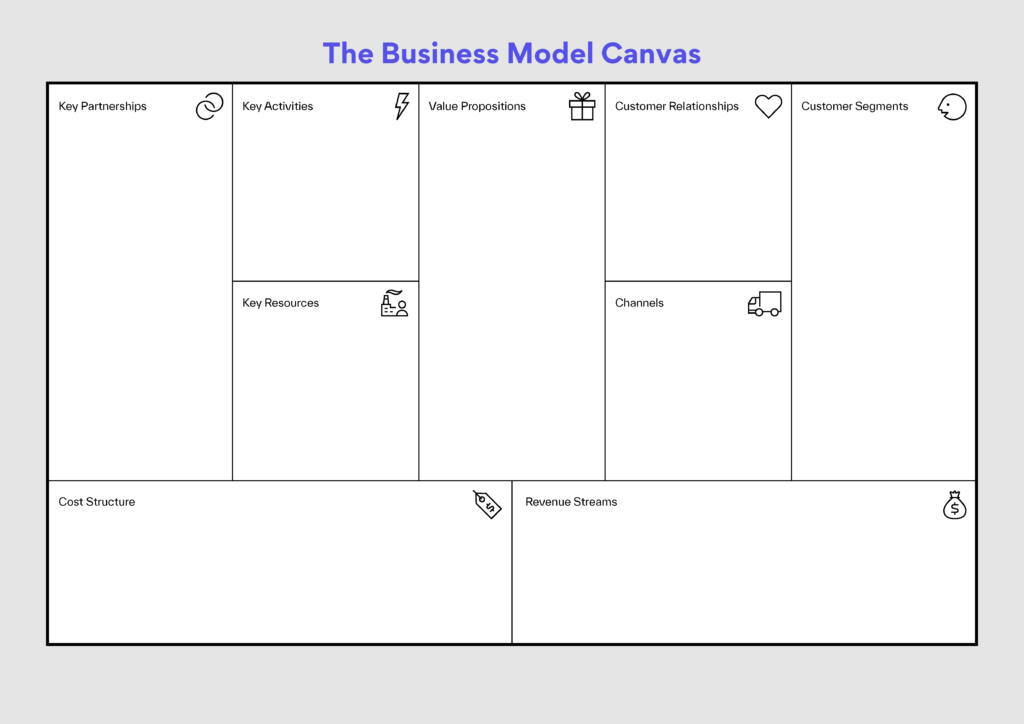

A good thing to also use is the business model canvas by Strategyzer – check out this great article on how to use it.

Benefits of a Business Plan

A well-crafted business plan provides clarity and direction for your business. It helps you stay focused on your goals, track your progress, and make informed decisions. Additionally, a business plan is essential when seeking funding, as it demonstrates to investors and lenders that you have a viable business model.

7. Assess and Plan for Risks

Identifying Industry-Specific Risks

Every industry has its unique set of risks. For example, businesses in the food industry face risks related to food safety, while those in the tech industry may face cybersecurity threats. Conduct a risk assessment to identify potential hazards that could impact your business.

Obtaining the Right Insurance

Business insurance is essential for mitigating risks and protecting your assets. Common types of insurance include general liability, professional liability, product liability, and property insurance. Choose coverage that aligns with the risks identified in your assessment.

Developing a Risk Management Plan

A risk management plan outlines strategies for minimizing and responding to potential risks. This plan should include procedures for handling emergencies, such as natural disasters, data breaches, or product recalls. Regularly review and update your risk management plan to address new risks as they arise.

8. Understand Your Tax Obligations

Types of Business Taxes

As a business owner, you’ll be responsible for various types of taxes, including income tax, payroll tax, sales tax, and property tax. Each tax has its filing requirements and deadlines, so it’s important to stay organized and compliant.

Payroll and Employee Taxes

If you plan to hire employees, you’ll need to understand payroll taxes, which include Social Security and Medicare taxes, federal and state unemployment taxes, and workers’ compensation. Payroll taxes can be complex, so consider using payroll software or hiring a professional to manage them.

Record Keeping and Compliance

Accurate record-keeping is essential for tax compliance. Maintain detailed records of all financial transactions, including income, expenses, payroll, and tax payments. This documentation will be invaluable during tax season and in the event of an audit.

9. Time Your Launch Strategically

Assessing Market Conditions

Timing is crucial when launching a business. Before you launch, assess the current market conditions to determine if it’s the right time to enter the market. Consider factors such as economic trends, industry growth, and consumer demand. Launching at the right time can significantly impact your business’s success.

Planning a Launch Timeline

Develop a timeline for your business launch that includes key milestones and deadlines. Consider factors such as product development, marketing campaigns, and legal requirements. A well-planned timeline ensures that everything is in place for a successful launch.

Being Decisive in Decision-Making

In business, time is often of the essence. While it’s important to make informed decisions, avoid getting stuck in analysis paralysis. As the saying goes, “done is better than perfect.” When you’re 80-90% confident in your plan, it’s usually time to pull the trigger.

10. Develop a Marketing Strategy

Understanding Digital Marketing Basics

In today’s digital age, a strong online presence is essential for any business. Familiarize yourself with digital marketing basics, including search engine optimization (SEO), social media marketing, email marketing, and content marketing. A well-rounded digital marketing strategy will help you reach a wider audience and generate leads for nearly any business model type.

Leveraging Social Media

Social media platforms are powerful tools for promoting your business and engaging with customers. Identify the platforms that your target audience uses most and develop a content strategy that resonates with them. Consistency is key, so establish a regular posting schedule and interact with your followers.

Measuring Marketing Success

Track the performance of your marketing efforts using key metrics such as website traffic, conversion rates, and customer engagement. Use analytics tools to gain insights into what’s working and what needs improvement. Continuously refine your marketing strategy based on these insights to maximize your return on investment (ROI).